Should You Sell a Stock After It Doubles? A Better Long-Term Investing Framework

One of the most common mistakes investors make is anchoring to past returns.

They say:

“I’m up 80%.”

“I doubled my money.”

“I’m up 200%.”

“So maybe I should just take the win.”

That feels logical. But it is often the wrong question.

The real question is not what the stock did for you from the past purchase price to today.

The real question is this:

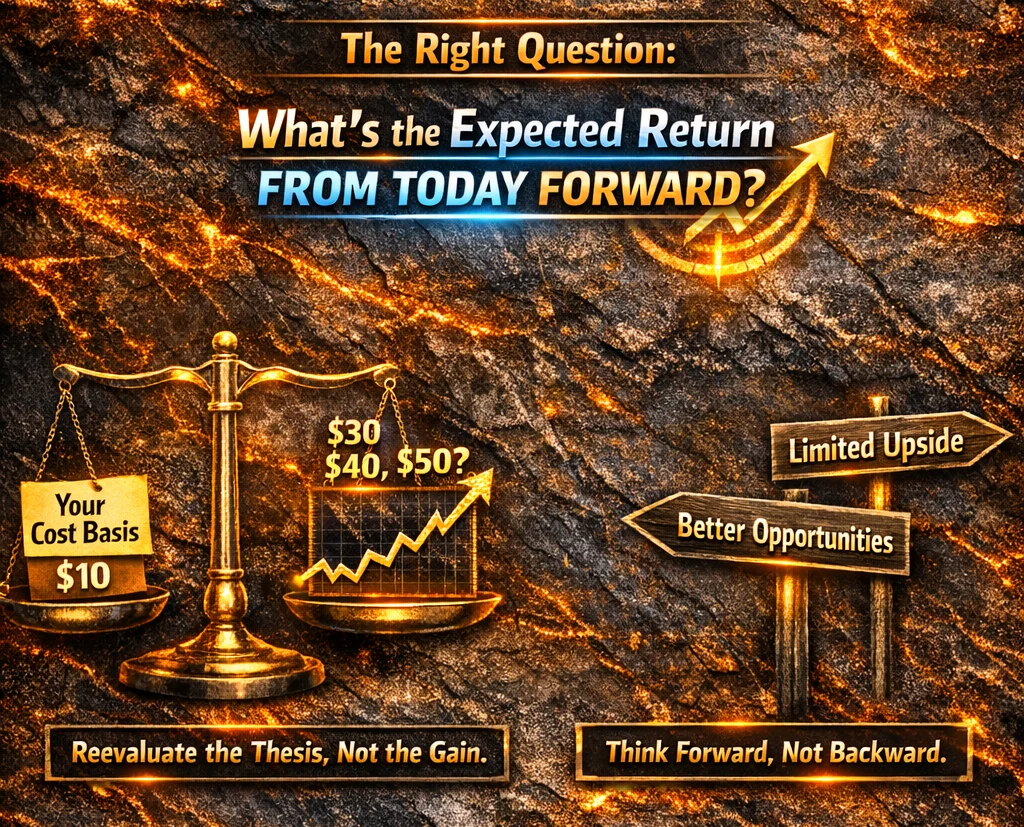

What is the expected return from today forward?

Your Cost Basis Is Not the Decision

Once you own a stock, your original purchase price becomes psychologically important but analytically less useful.

A stock that went from $10 to $18 can still be a great hold if it can reasonably go to $30, $40, or $50 over the next few years. In that case, selling just because you have a gain may actually destroy value.

On the other hand, a stock that doubled might now be close to fair value. If upside from here looks limited and better opportunities exist elsewhere, then selling can make sense.

This is why strong investing requires re-underwriting the business again and again.

Reevaluate the Thesis, Not the Gain

A smarter framework is to revisit the company every quarter or after major developments and ask:

Has the business improved?

Has valuation outrun fundamentals?

What does my projection say from today?

Is this still one of my best opportunities?

That framework works for winners and losers.

If a stock is down sharply but the forward return still looks excellent, holding or adding can make sense. If a stock is up sharply but future return now looks mediocre, trimming or exiting may be the better move.

The decision is always made from the present.

Why Stop Losses Often Hurt Long-Term Investors

This is where long-term investing differs sharply from trading.

Stop losses are usually designed for traders. They can make sense in strategies built around price action, momentum, and tight risk controls. But for long-term investors, they often create bad outcomes.

Why?

Because great businesses can be very volatile in the short term. A sharp market selloff can push a stock down 10%, 15%, or 20% temporarily, trigger the stop loss, and then reverse quickly. The investor gets forced out, misses the rebound, and may even create a taxable event in the process.

That is not real risk reduction. It is often just mechanical damage.

Long-Term Investors Need Conviction, Not Triggers

If your research is strong and the business is intact, lower prices can actually be opportunities.

That does not mean buying every dip blindly. It means that price declines should be interpreted through the thesis, not through automated panic. Long-term investors often scale into positions as prices get more attractive precisely because they understand the business better than the short-term market does.

A stop loss can work directly against that mindset.

A Better Sell Framework

Instead of asking, “Should I sell because I’m up a lot?” ask:

- What is my realistic upside from here?

- What are the bear and base cases now?

- Has valuation become stretched relative to growth?

- Would I buy this stock today at this price?

- Is there a clearly superior opportunity elsewhere?

Those questions are much more useful than anchoring to a percentage gain.

Final Thoughts

You do not sell a stock because it doubled.

You sell a stock because the forward opportunity no longer looks attractive enough relative to the alternatives.

And you usually should not use stop losses as a substitute for judgment if you are a true long-term investor.

Past performance on your position is history.

Your job is to evaluate the next chapter.

That is how disciplined investors hold great winners longer, exit weaker opportunities faster, and avoid getting shaken out by noise.