What Is a Reasonable P/E Ratio? How to Match Valuation to Earnings Growth

One of the most common questions in investing is this:

What is a reasonable P/E ratio?

The answer is not a single number.

A reasonable price-to-earnings multiple depends on context. Business quality matters. Margins matter. Predictability matters. Cyclicality matters. But one of the most important starting points is earnings growth.

In other words, valuation should not be judged in isolation.

A multiple only makes sense relative to what the business is likely to earn in the future.

The Mistake Investors Make With P/E Ratios

A lot of investors see a low P/E and assume cheap.

They see a high P/E and assume expensive.

That is far too simplistic.

A company growing earnings at 5% a year should usually trade very differently from a company growing earnings at 25%, 35%, or 50%.

The market knows this. That is why better businesses often deserve higher multiples.

The real question is not:

Is this P/E high or low?

The real question is:

Is this P/E justified by the company’s future earnings power?

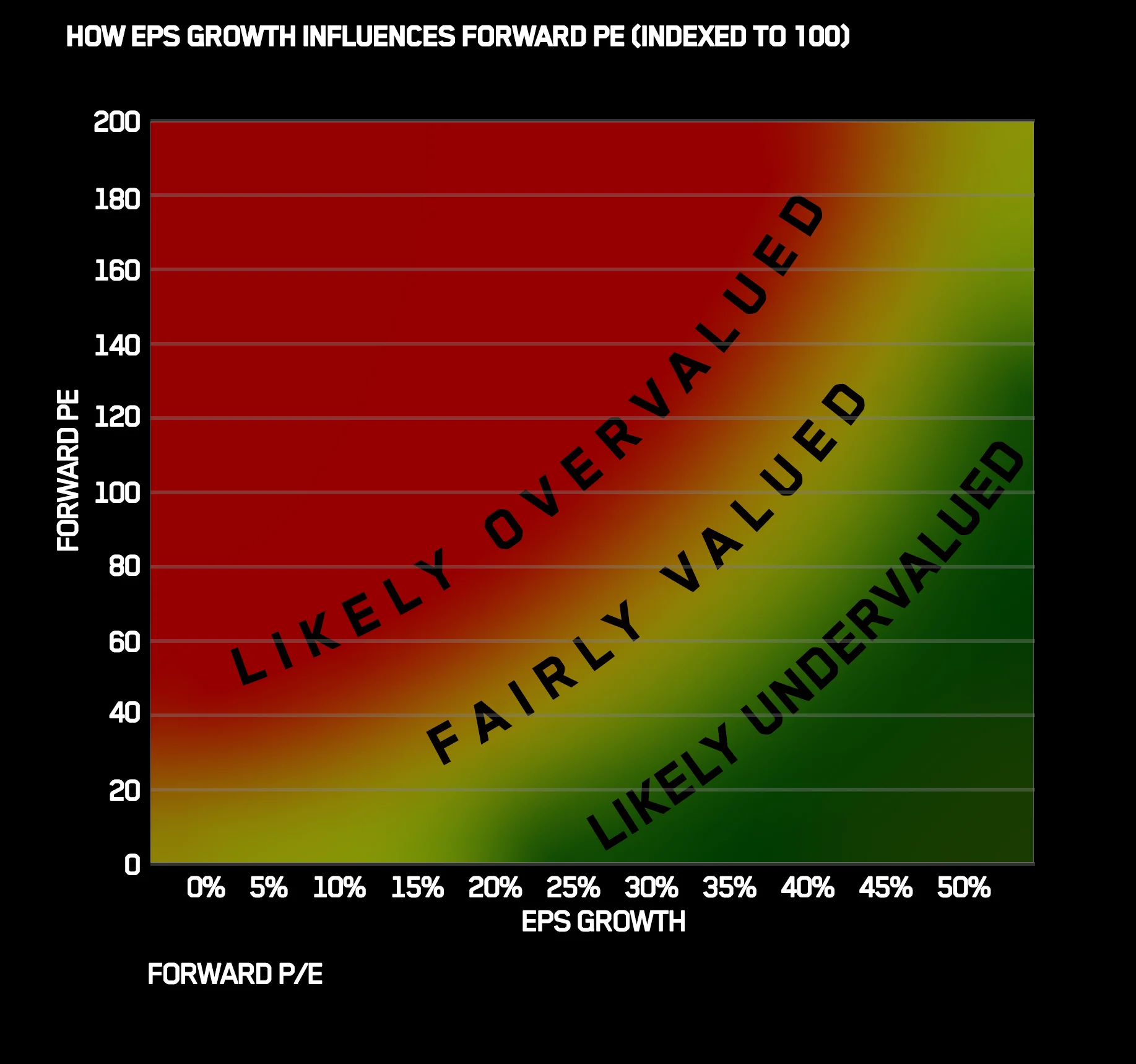

A Practical Rule of Thumb

A useful mental model is that a fairly priced company’s P/E ratio often roughly tracks its earnings growth rate over time.

That does not work perfectly in every situation, but it gives investors a powerful anchor.

For example:

- a slower-growing company might deserve a more ordinary multiple

- a business growing EPS around 25% could justify a meaningfully higher multiple

- a company growing earnings around 35% annually may deserve something in that neighborhood, assuming the quality is real

This way of thinking stops you from blindly paying any price for growth, while also preventing you from undervaluing genuinely exceptional businesses.

Growth Must Be Real, Not Promotional

The key word here is earnings.

Not hype.

Not adjusted storytelling.

Not vague promises.

The growth that matters most for valuation is real earnings growth, ideally supported by:

- improving revenue

- healthy margins

- credible assumptions

- durable demand

- realistic reinvestment economics

A company may sound exciting, but if the earnings path is weak or highly uncertain, the “reasonable” multiple should come down.

Valuation should reward evidence, not fantasy.

Why Conservative Assumptions Matter

One of the best habits in valuation is being conservative.

Do not build a model that assumes everything goes right.

Do not pay for market mania in advance.

Do not assume the future multiple will expand forever.

A smarter approach is to:

- estimate future earnings using realistic assumptions

- assign a reasonable range of possible P/E multiples

- see whether the stock still offers attractive upside without needing perfection

That keeps your framework grounded.

A great investment should work even if enthusiasm cools.

You want upside from business performance, not just from crowd excitement.

Business Quality Still Matters

Two companies with the same earnings growth rate may not deserve the same P/E.

Why?

Because not all growth is equally valuable.

A predictable subscription business with strong margins and recurring revenue may deserve a premium multiple because the earnings stream is more reliable.

A cyclical company with weaker visibility may deserve a lower multiple, even if short-term growth looks similar.

That is why valuation always needs a second layer:

not just how fast the company is growing, but how durable and trustworthy that growth is.

Signs the P/E Might Be Too High

A valuation may be stretched when:

- the P/E assumes years of perfect execution

- growth expectations are already extreme

- margins have little room to improve

- the business is cyclical but priced like software

- investors are paying for excitement rather than results

In these cases, the company may still be great, but the stock may be too crowded.

Signs the P/E Might Be Reasonable or Attractive

A valuation may be reasonable when:

- earnings growth is strong and credible

- assumptions are conservative

- the business has durable demand

- margins support future EPS expansion

- the multiple is sensible relative to growth

- you do not need euphoric sentiment for the investment to work

That is usually the kind of setup long-term investors should be hunting.

Final Thoughts

A reasonable P/E ratio is not about memorizing one market number.

It is about matching valuation to growth.

Start with earnings growth.

Layer in business quality, margins, predictability, and cyclicality.

Use conservative assumptions.

And never rely on hype to justify the price you are paying.

Because valuation is not about finding stocks with low numbers.

It is about finding businesses where the price still makes sense relative to the future you reasonably expect.